Mid-year optimism, and chokepoint management

The review; Gulf, trade, inflation, a chokepoint world, Semis; the mother of all chokepoints

Mid-year review

Taking stock as we approach mid-year 2026. Reviewing thematic progress, and strength of growth tailwinds from frameworks grounded in reality, as opposed to the verbose and conjecture-based political narratives. Conjuring up a degree of optimism for 2H-26.

Gulf

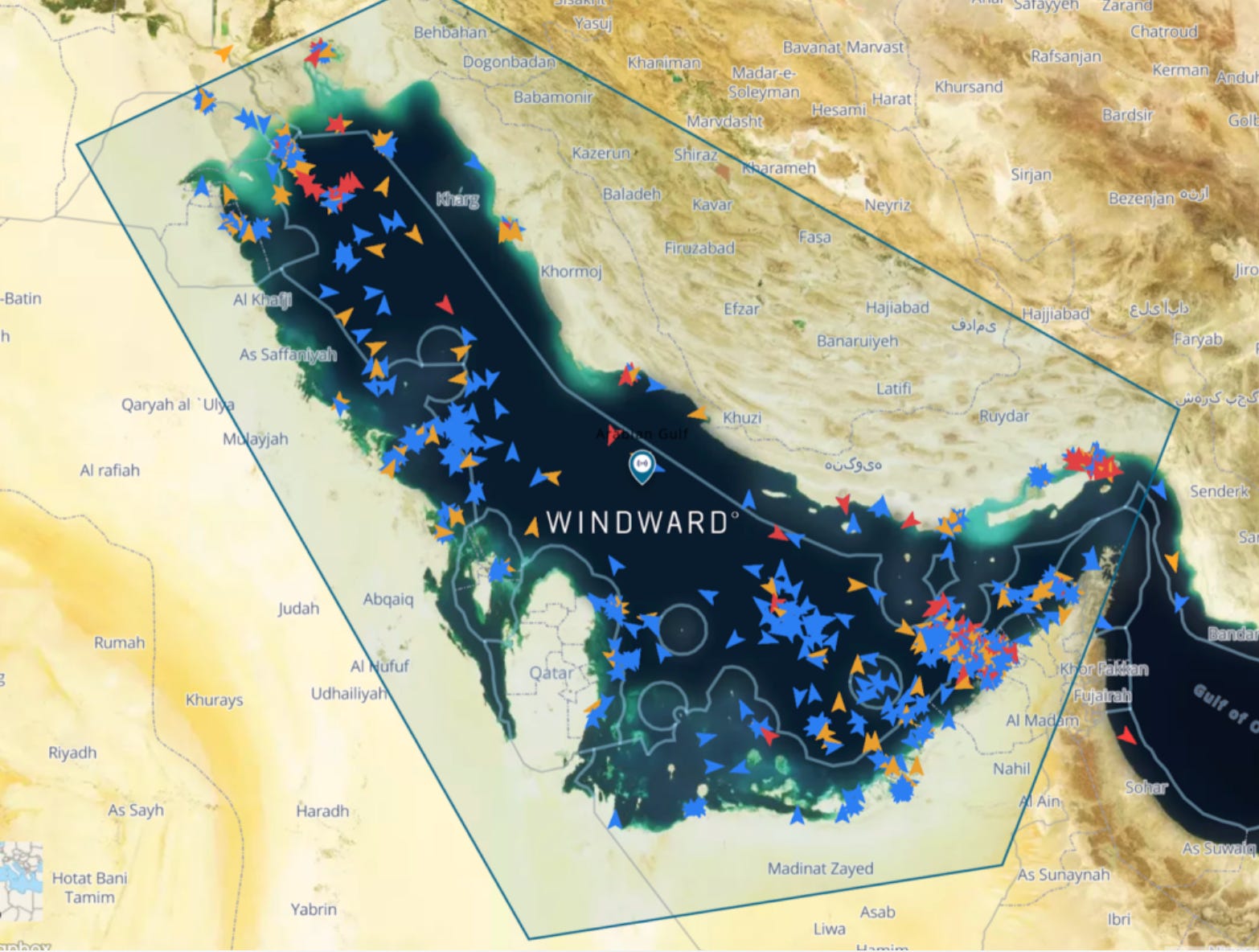

Firstly, on the Persian Gulf conflict, viewing the impressive & compressed timeline, and within a Strategy of Denial framework, progress remains sufficiently on track. Oil prices remain elevated, with 160 oil tankers still stuck inside the SoH, and a further 50 LNG-LPG carriers idle/stuck as well. This keeps anxieties high, but progress in reshaping the post-conflict ME dynamic continues.

So far globally, most nations have chosen to draw down stockpiles or pay a bit of ransom to the IRGC rather provide naval escort for their merchant fleet.

The media narrative treats this as an immoveable constraint when it is actually an economic choice. The US ended hostilities, agreed to a ceasefire with Iran, UN passed resolution 2817 upholding Freedom of Navigation (11 March), allowing countries to defend their ships, and yet the world still did nothing.

The media prefers to frame this as some kind of US military failure, while the reality is, the world needs to read up on the Strategy of Denial doctrine. This defines the US’s measured global power projection now. It denies enemies and adversaries leverage and certain threat levels, but it is not a global police force. Other countries must provide security for their own people, their own commercial fleets, and they must restructure their own global supply lines. The US won’t be doing this for them.

The announcement over the weekend of Trump’s broad regional leadership call that resulted in a MOU towards a peace deal with Iran, fell along the lines I proposed early on in the conflict (15 Mar). The GCC countries + regional military powers have all signed on to take this leadership role. The US doesn’t want responsibility for keeping peace in the region. It simply wanted to level the hard power playing field and eliminate Iran’s nuclear program. The peace framework was always going to require GCC and regional leadership to succeed.

While another 60-day extension to the ceasefire sounds tortuous, if the ships are passing through the straight and the transport backlog is clearing, the world will be far more patient than it has been these past 2 months. Market focus will migrate elsewhere. This is positive news for risk appetite.

Tariffs & trade

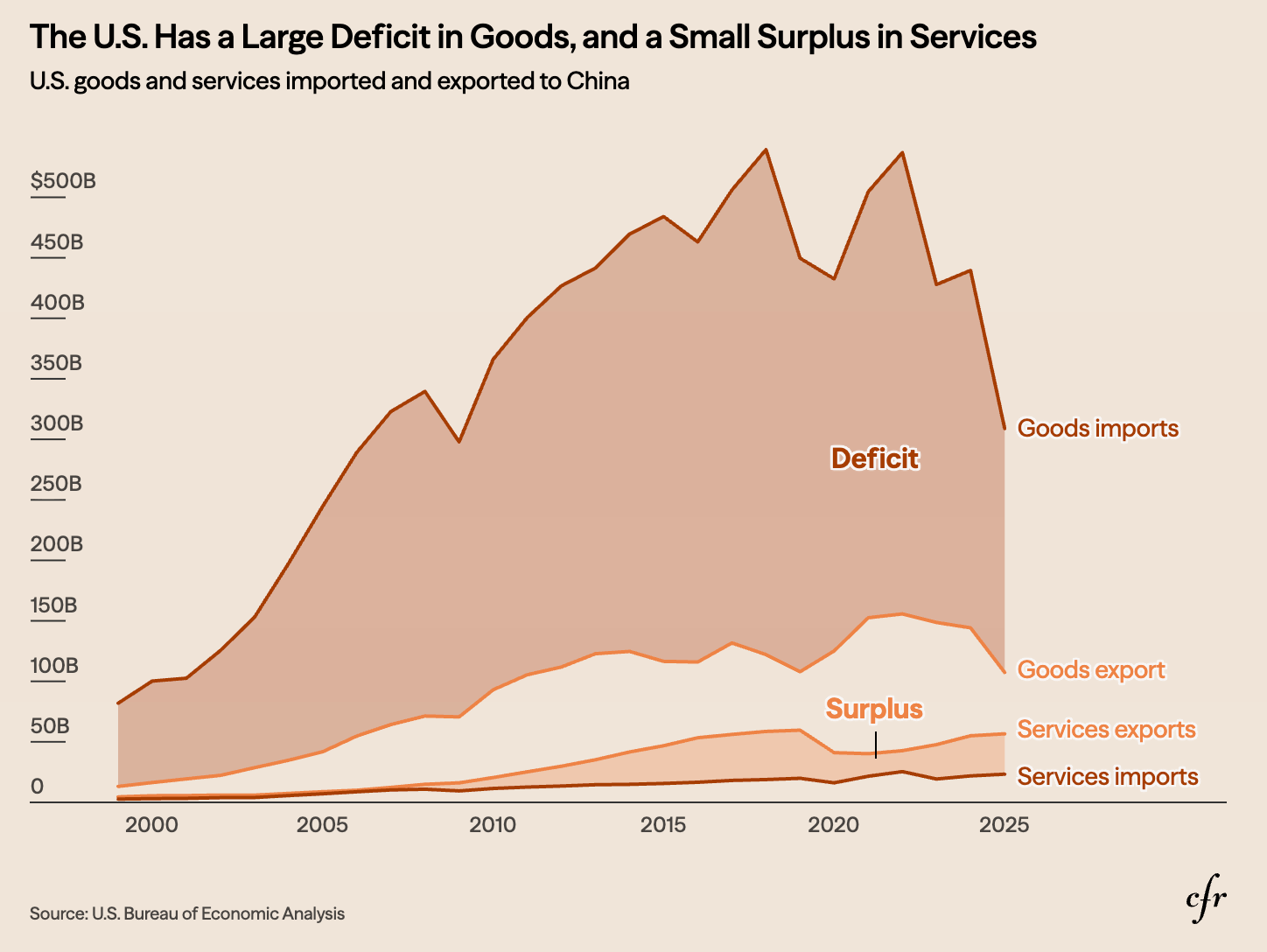

On the issue of tariffs and trade wars, the year over year effects are beginning to drop out, modified trade is settling into its new equilibrium. The China excess capacity dump from 2024-25 has peaked and is now declining. The ROW has made many of the basic trade-offs necessary to align with US tariff objects vs China, or independently attempted to recalibrate their bilateral trade with China.

The US is still pursuing a grand bargain with China, floating various versions of a Board of Trade, and a Board of Investment. The recent Xi-Trump summit in Beijing has advanced the new framework of Strategic Stability. The critical mineral export control truce was extended/augmented (WH Factsheet) beyond the Nov-26 expiry, giving more time for the US (and others) to innovate their way out of the problem. Effective tariffs on China are down to 30% now, compared to levels above 100% this time last year. It has been 12 months of progress.

Central banks & inflation

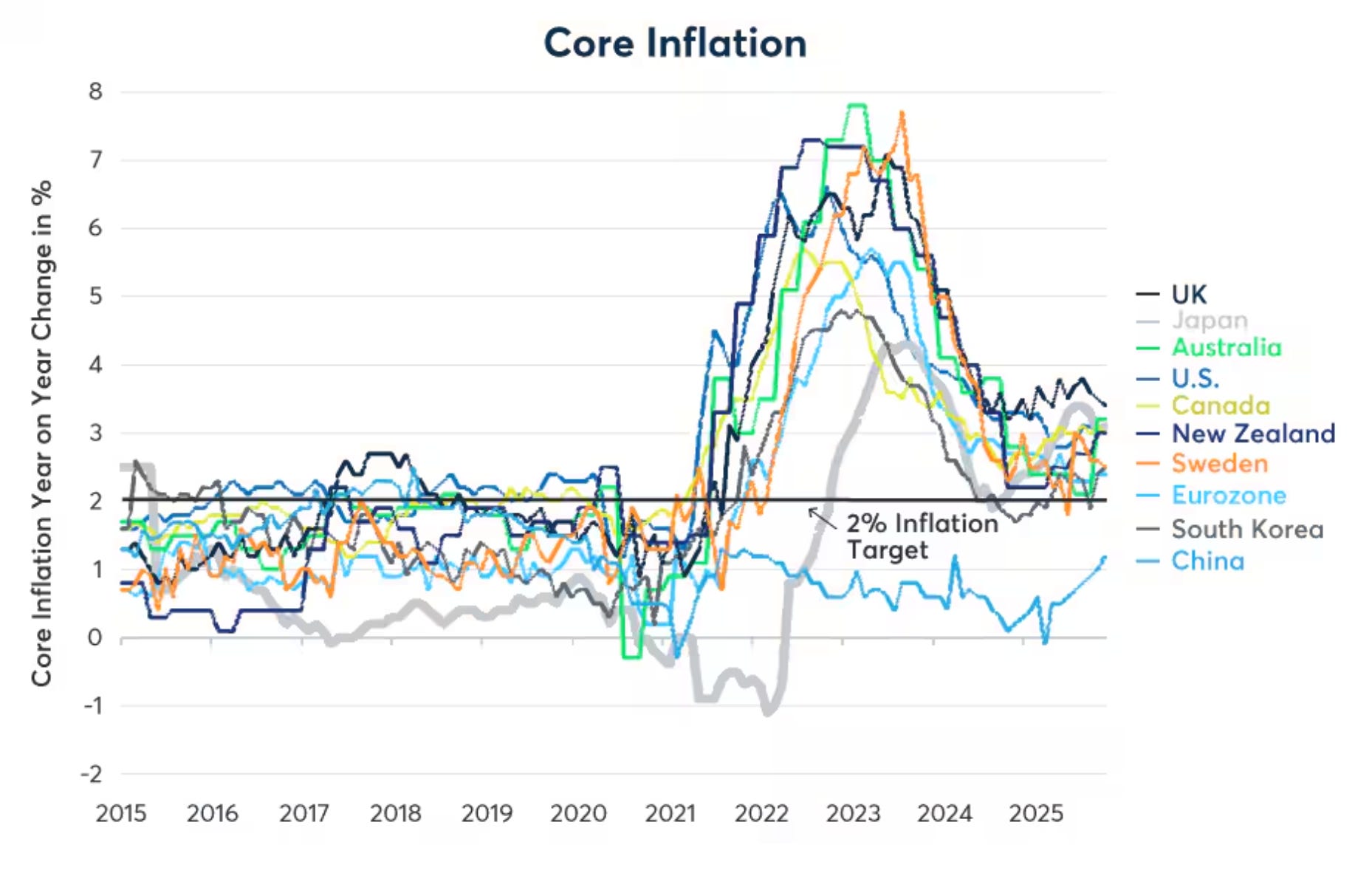

Central bank policy is another area where a mid-year update is necessary, as the Fed gets its new Chairman and global inflation receives another kick higher from another energy shock.

There are not a lot of success stories out there. First, central banks spent the disinflation-psychology dividend early on amid a post-Covid surge in prices, then it tried to ignore a broad external supply shock from the Russia-Ukraine war in 2022, then it sought to pre-emptively cut rates in search of growth before inflation returned to target in 2024, believing that mean reversion forces were unchanged from the previous decade.

An end to disinflationary forces like globalisation, and a transition from efficiency to resilience as the defining global supply chain mantra, caught the central banks out . . . again. They were busy risking their multi-decade credibility on a goldilocks inflation soft-landing, when President Trump took office again in 2025 and began disrupting what was left of the status quo. This has perpetuated the impression that central banks are routinely behind the curve now. Global shocks keep coming and policy has not successfully anchored inflation expectations.

The worst offender has been the BoJ, as it failed to keep to a normalisation pace sufficient enough to get rates to neutral before the next inflation shock hit. It only managed 3 rate hikes up from zero in 2 years.

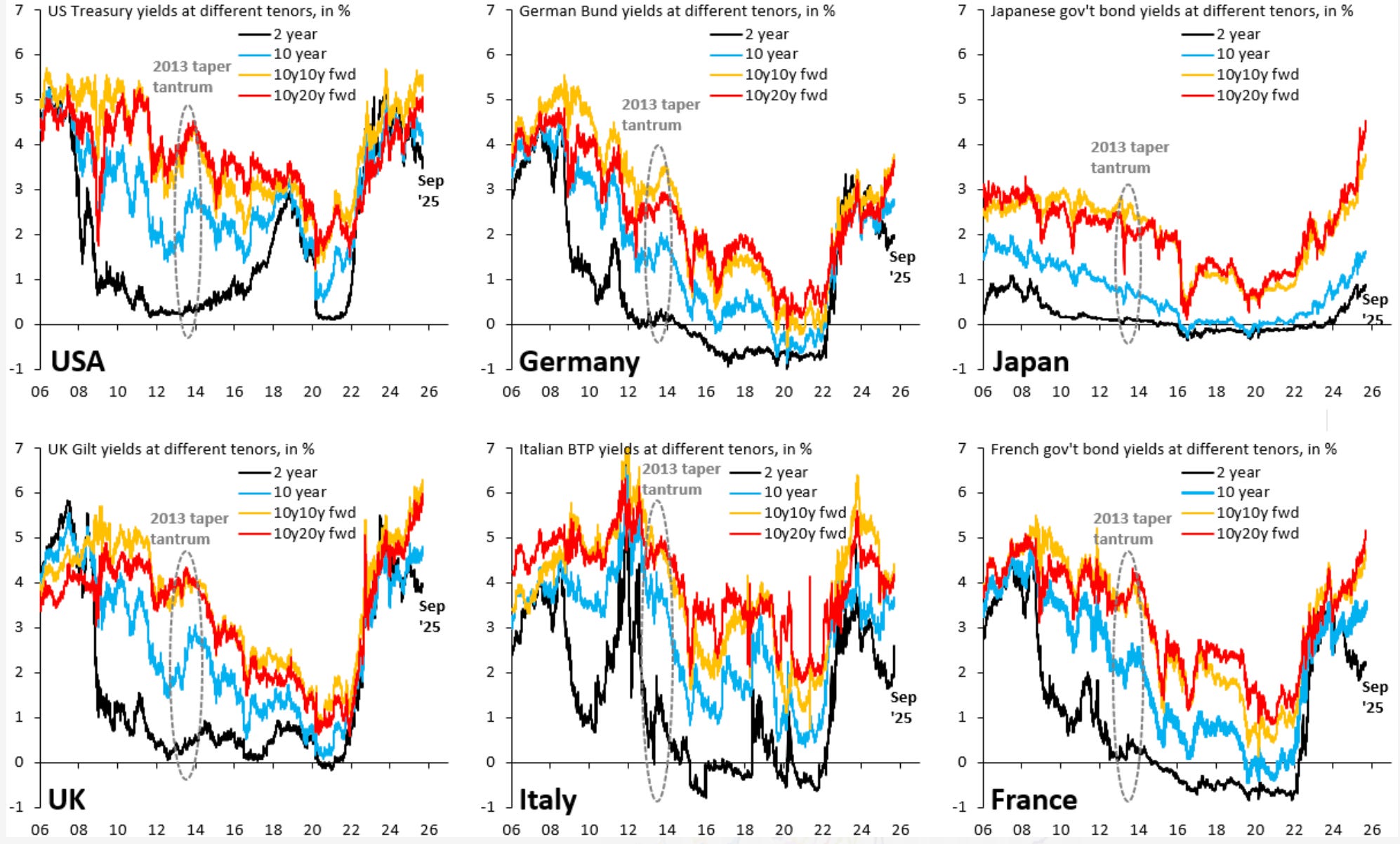

Most other central banks managed to restore real rates sufficiently before this latest energy shock hit, but the market penalty has still come via LT inflation expectations and bond market term premium. Previously compressed spreads and renewed fiscal concerns certainly have played a part in the move higher, but few countries truly showed signs of tight monetary policy before the shock hit.

Will a Warsh Fed have an impact beyond the US? I think he will. The change of framework, and the change of big picture view that Warsh will try to instil within the FOMC will resonate with many central bankers globally. Central banking circles are quite collegiate, and good ideas will cross pollinate quickly. A hard-money inclined Fed Chair is something the world hasn’t seen for a long time.

Even if the market remains skeptical for the first year (as they should), eventually, data will validate the approach. Higher short term real rates will eventually flatten the yield curve, validating a successful transition. But first the Fed must deal deftly with the current short term inflation risks (at least one rate hike), downsize the balance sheet, collaborate with Treasury on GSE privatisation, integrate tokenisation & stablecoins, and lower regulatory friction for banks. Compressing inflation through domestic efficiency rather than globalised efficiency is the new playbook.

A Chokepoint view of the world

As the world reels from one chokepoint lesson after another, eventually it will start to see chokepoints everywhere. True chokepoints, ie, those bound by natural laws and geography, are hard to hedge, but still, hedges exist.

The best remedy for all chokepoint risk is time. With time, countries can adjust strategy, develop alternatives, improve diversification. This time-buying strategy has featured prominently through the Russia-Ukraine war shock, Trump tariff shock, China critical minerals shock, and with the current SoH shock.

Given that these shocks hit energy, mining, and critical inputs markets strongly, one of the simplest responses has been hoarding, stockpiling, and buffer building. Even Covid triggered hoarding of certain medical supplies. The problem with hoarding as a strategy, eventually, once the crisis has subsided, these stockpiles become expensive and deflationary forces. They compress profit margins and weigh on investment.

While categorised different (national reserves, precautionary reserves, strategic reserves, import buffers), they are essentially excess inventory. The stockpiling strategy eventually hits an economic limit, no matter how volatile the geopolitical arena. Barring out-right war, stockpiles eventually reach an economic peak. The problem is that this peak differs greatly between state-owned economies vs free market economies.

State-owned economies hoard and stockpile as a general operating rule. They rarely have to transparently account for these types of inefficiencies. In free market economies, the drag on performance is quickly revealed, and the new tolerable buffers find their economic equilibrium. No where is this more evident than in chokepoints that are driven by cost and innovation hurdles. Scarcity driven by proprietary, competitive advantage is unique amongst the chokepoint dilemmas. This is what makes the semiconductor & AI space such a powerful geo-economic arena.

Semis, a different kind of chokepoint

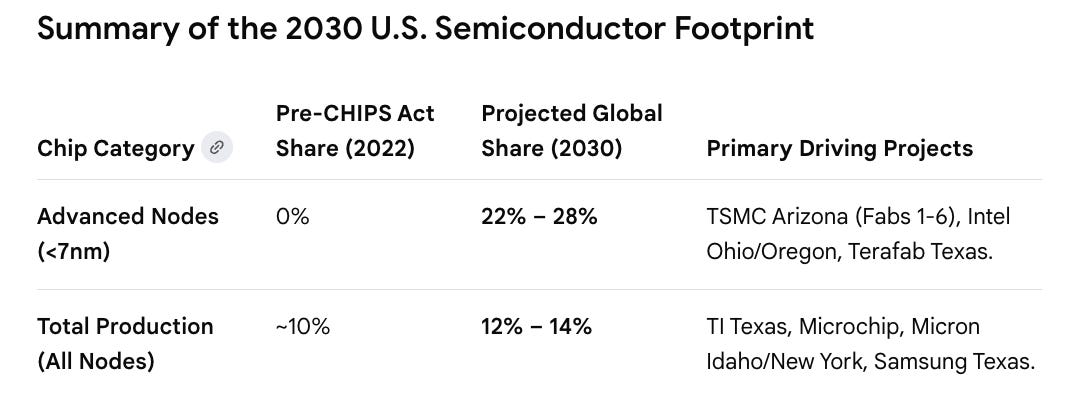

At the moment, Taiwan is a single country chokepoint for semiconductor chips, which lends itself to some of the traditional chokepoint analysis; China blockade or forced integration risk. However, the core of this issue is a technological one. Taiwan began offshoring 5-6 years ago, with TMSC’s Arizona and Kumamoto projects representing the consequential dimension of this strategy.

Not only did Taiwan chose two strategic destinations geographically (China’s primary rivals), but it chose two top manufacturer/consumer markets for these highest-end technologies. Innovation will therefore eventually drive virtuous cycles in both of these locations, forming new ecosystems that are part of the Taiwan elite’s geopolitical hedge, and the host nation’s strategic arsenal.

TSMC manages 16 Fabs world-wide, with 11 of them, and the primary hubs in Taiwan. It has 2 new Fabs in the US, 1 in Japan, and 2 in China. The Arizona project will see a further 3 Fabs added, including a cutting edge 3nm-capable Fab. One more Fab for Kumamoto, and Germany also just broke ground with its first TSMC joint venture, targeting automotive microcontrollers.

The point is that by 2030, the US will have gone from 13% of total semi production globally to over 25%, and Japan will have increased its share to 15%. This is how the chokepoint is being managed. But demand for AI investment has created a subcategory of its own.

For the ultra-advanced, high-performance logic processors (nodes under 7-nanometer and 3-nanometer), manufacturing concentration in Taiwan is even higher, over 90%. TSMC is building 3nm Fabs in Arizona and Kumamoto, but the majority will still be in Taiwan.

This is why innovation and new entrants are the only true solution to this technology chokepoint. Samsung’s 3nm chips and Intel’s sub 2nm are adding competitor depth, as will xAI’s TeraFab collab with Intel.

But the world needs time disburse the over-concentration in Taiwan. Seen from this perspective, one can understand why managing the cross Strait risk with China is the intelligent play. The world needs about 5 years to dilute the chokepoint.

The TSMC Arizona Project is now up to $165bln, while Kumamoto is a further $20bln. It is sending up to 3,000 highly skilled engineers to the US to manage this mega project, and 400+ to Japan. The Arizona project is built to service the supercomputer & AI value chain, while the Kumamoto project initially started its focus on the Industrial, Automotive, Edge AI value chain, and has since seen an upgrade with the second Fab to meet surging AI-related demand.

This is the largest offshoring, geopolitical hedging investment plan in history. Years in planning, with long lags, and a heavy diplomatic responsibility to keep the waters calm in the interim. Compared to a 3 months shipping bottle neck in the ME, this level of chokepoint management is 10x levels higher in complexity.

Fortuitous execution

Successful execution of these strategic plans and logical cross-border investments between allies at this ultra-high level of tech is cause for optimism. This is what keeps risk appetite strong, this is what drives the tech stocks higher year after year.

There are so many ways for either the general environment, or the politics, or actions of rivals to disrupt this ascending wave. Every time we successfully cut the tail risk off a kinetic conflict, or avoid a diplomatic disaster, or find bilateral common ground with our allies, this is an opportunity to cheer. This feeds the optimistic scenario. Organic transitions in the new world order are happening.

The task doesn’t get easier, but the level of energy displayed, and some of the impressive wins recorded reflects excellent work by skilled practitioners. The collection of corporate leaders in US, Japan, Taiwan, and South Korea at this particular moment, and those that have lent their global expertise to the public sector, is of the highest level.

The bureaucracy may still be a drag, and public sector investment may still have multiples of less than 1, but the idea generation, and the public-private partnership to see it implemented has never been this impressive in my life time. I stand amazed.

I keep voting with my dollars, and they keep validating my good faith. Looking for more gains in the second half of 2026.

Thanks, Mark.